Buying a home is one of the most exciting milestones of your life. To prepare yourself for this moment, you need to know what to expect during the process. This step-by-step first time buyer’s guide created by your agent will help reduce the stress of buying a home and help you enjoy the journey as much as possible.

My goal is to provide you with the most personalized service that is designed to help you buy your dream home

Helping you review and choose your best home loan product is what we do.

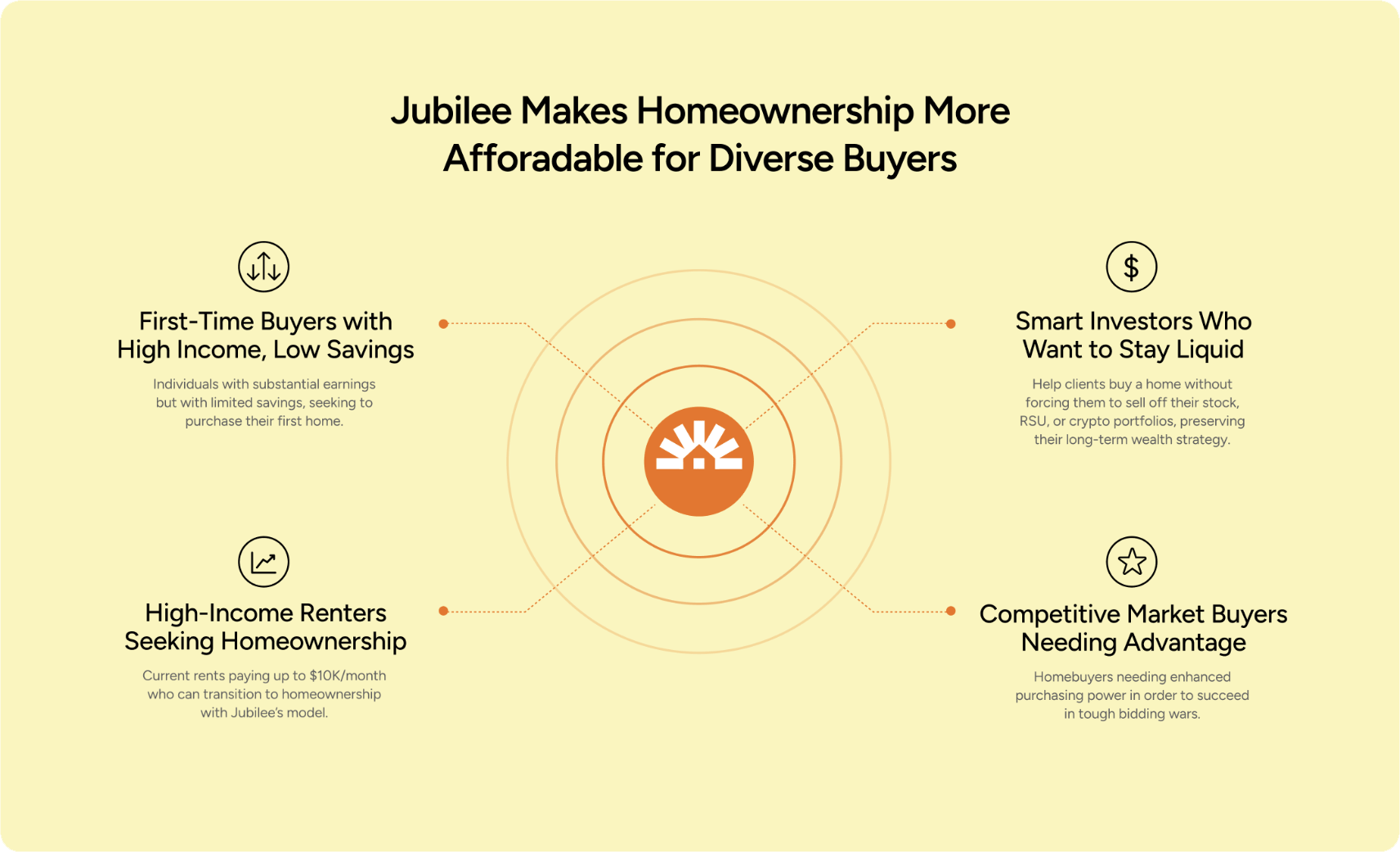

No matter your financial situation, we can help.

HOW WE CAN HELP:

HOW WE CAN HELP:

HOW WE CAN HELP:

HOW WE CAN HELP:

HOW WE CAN HELP:

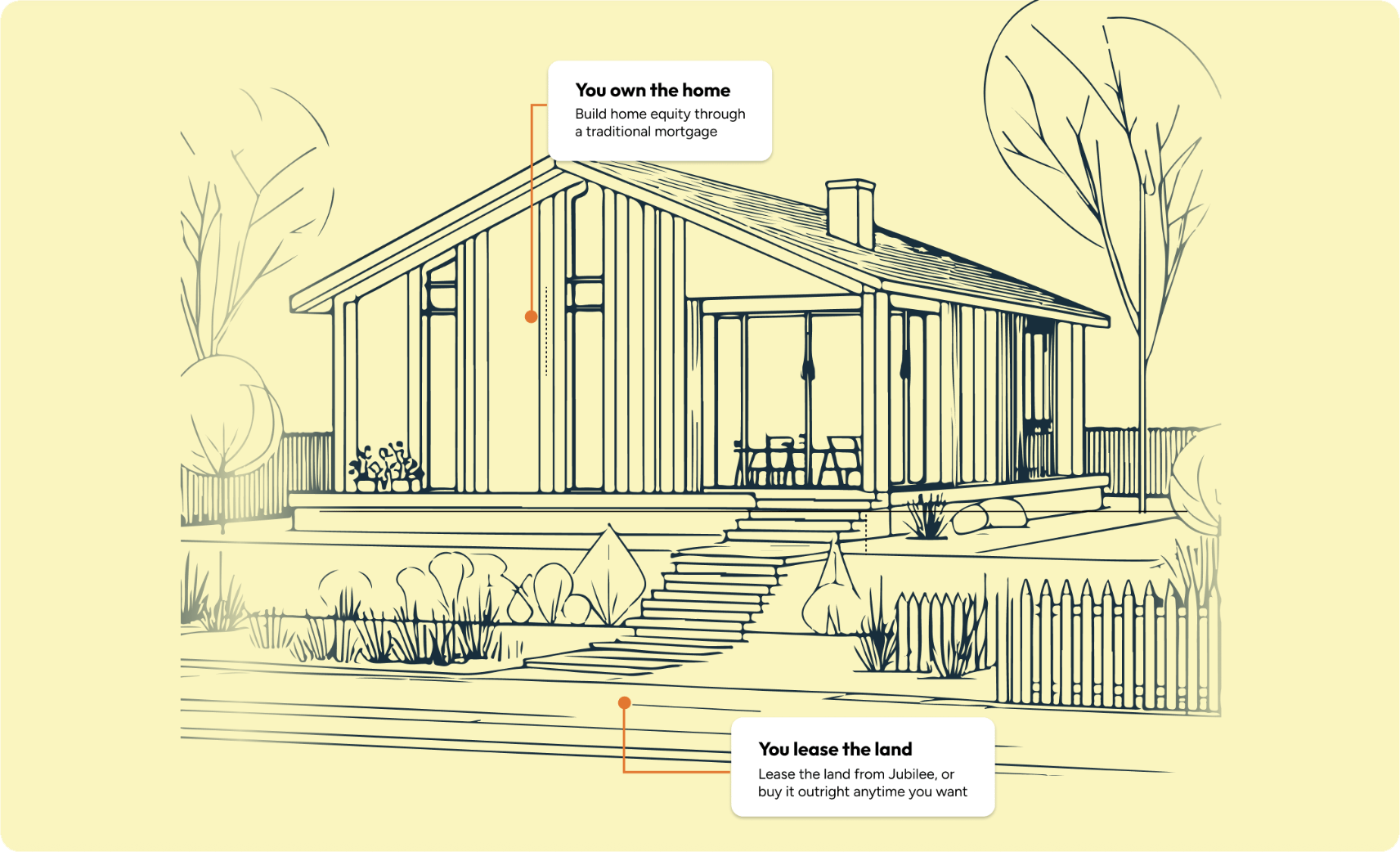

Jubilee separates the cost of the property, so you can buy the home you want sooner-build equity from day one.

Work with your agent, they represent you and Jubilee.

We partner on the purchase, you fully own the home on day one.

You can purchase the land on your timeline.

If this sounds like you, then a leasehold property may be a great fit:

A leasehold, on the other hand, means you own the building or home for a long period of time through a lease, but someone else retains ownership of the land. Think of it like a long-term rental, but with a significant difference: you own the structure! Instead of buying the land, you lease it, often for many decades (common terms are 30, 60, or even 99 years).